Production-grade time series toolkits that blend probabilistic models, deep learning, and dependency modeling while enforcing strict engineering discipline.

Overview

Interactive Analysis

Overview

This section aggregates every advanced methodology that complements the Udemy curriculum. Each chapter represents a different modeling philosophy—state-space, Kalman filtering, Prophet, LSTM, tree-based ML, wavelets, and copulas—yet all of them share the same safeguards: walk-forward retraining, validation-separated feature engineering, metadata exports, and reproducible signal pipelines.

Engineering Principles

Walk-forward training/backtesting with no look-ahead bias.

Strict separation of train/validation/signal generation code paths.

Production safety hooks such as logging, retries, fallbacks, and metadata export.

Signals are shifted by one bar to ensure trades only use information up to t-1.

Shared utilities (`utils/backtest.py`, `utils/data_loader.py`) keep every chapter consistent.

Learning Objectives

Track time-varying betas via state-space models.

Implement four Kalman filter approaches: Custom (educational), FilterPy (production with adaptive noise/EKF/UKF), PyKalman EM (parameter learning with credible intervals), and Particle Filter (non-Gaussian robustness).

Operate Prophet for seasonality-aware forecasts with configurable retraining cadence.

Train LSTM classifiers that avoid leakage, address class imbalance, and auto-select thresholds.

Deploy XGBoost binary classifiers for direction prediction with rich technical features, ROC-based optimal threshold selection, and feature importance analysis for interpretability.

Generate wavelet-based multi-resolution features for denoising and volatility clustering.

Model joint distributions with Gaussian/Clayton copulas and feed scenarios into risk-aware backtests.

Chapter Highlights

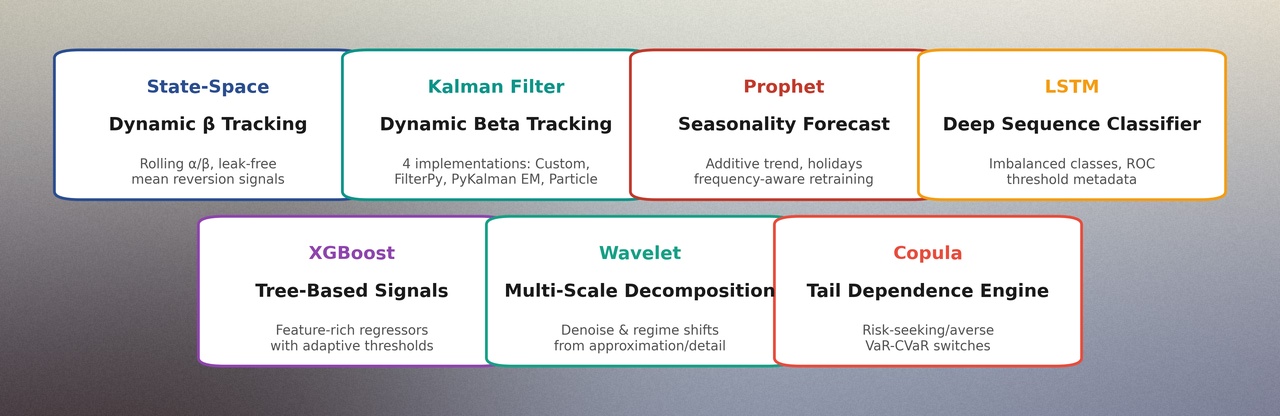

Chapter 1 — State-Space Models

Theory: β(t) follows a random walk while TQQQ returns track NASDAQ via time-varying α and β.

Implementation: `state_space_model.py` computes rolling α, β, and tracking error in vectorized pandas.

Backtest: β deviations trigger mean-reversion trades with all signals delayed one bar.

Chapter 2 — Kalman Filter

Theory: State-space estimation with four complementary approaches: Custom (from-scratch), FilterPy (production-ready with adaptive noise), PyKalman EM (parameter learning via EM), and Particle Filter (Monte-Carlo for non-Gaussian cases).

Implementation: All four implementations estimate time-varying alpha/beta for TQQQ vs NASDAQ. Custom provides educational value, FilterPy offers EKF/UKF support, PyKalman EM learns covariances and provides credible intervals, and Particle Filter handles non-linearities via resampling.

Applications: Price trend extraction (state: [price, velocity]) and dynamic beta tracking (state: [alpha, beta]). Each implementation demonstrates different trade-offs between educational value, production readiness, parameter learning, and robustness to non-Gaussian noise.

Chapter 3 — Prophet Model

Theory: Bayesian additive regression with decomposed trend, seasonality, and holiday components.

Implementation: Rolling forecast cache with retrain cadence and metadata logging.

Backtest: Compare Prophet forecast bands against last close; trades execute only on next bar.

Chapter 4 — Deep Learning (LSTM)

Theory: Sequence-to-label classification over normalized log returns.

Implementation: Class weights + ROC-threshold selection; weights and scalers stored per ticker.

Backtest: Probabilistic signals thresholded by stored optimal cutoff, then shifted by one day.

Chapter 5 — Tree-Based ML (XGBoost)

Theory: Binary classification for direction prediction (up/down) using gradient boosted trees. XGBoost stacks multiple weak decision trees, improving them step-by-step based on residuals. Unlike LSTM which learns temporal patterns from sequences, XGBoost leverages interpretability and feature importance analysis by considering various technical indicators simultaneously.

Implementation: `create_features` generates rolling returns, volatility, RSI, moving averages, and momentum features with lag features and rolling statistics to capture temporal patterns. The model uses `scale_pos_weight` to handle class imbalance and implements a two-stage training process with early stopping. ROC curve finds optimal threshold, and top 10 feature importance plus performance metrics are saved as metadata JSON.

Backtest: Signals generated based on predicted up-movement probability. Buy if probability exceeds optimal threshold, sell if below one minus threshold. All signals shifted one day later to prevent look-ahead bias. Walk-forward backtest visualizes cumulative returns, Sharpe ratio, drawdown, and trade history.

Key Advantages: High interpretability with immediate feature importance visibility, fast training, relatively simple hyperparameter tuning, and ability to explain predictions using SHAP values or partial dependence plots. Suitable for factor scoring or credit risk early warning systems where multiple indicators need simultaneous consideration.

Chapter 6 — Wavelet Transform

Theory: Discrete wavelet transforms for multi-scale analysis and denoising.

Implementation: `pywt` pipelines reconstruct approximation/detail coefficients without leakage.

Backtest: Use spreads between raw price and low-frequency component to detect stretched regimes.

Chapter 7 — Copula Models

Theory: Separate marginal distributions from dependence structure (Sklar’s theorem).

Implementation: Clayton/Gaussian copulas for tail diagnostics, Monte Carlo scenario generation.

Backtest: VaR/CVaR-style triggers react to changing joint risk and feed a dual-strategy engine (risk-averse vs. risk-seeking).

Common Backtest Methodology

Chronological 70/30 train-test splits with optional walk-forward retraining.

Signals delayed by one period; price alignment handled by shared `walk_forward_backtest` helper.

Performance pack: equity curves, Sharpe, drawdown, win-rate, and trade blotters.

Metadata + artifacts (models, thresholds, scalers) saved per chapter for reproducibility.

Status & Notes

The code is production-ready today, while the Udemy lecture series for Section 4 is still being finalized. All scripts are educational samples—re-run training locally, validate assumptions, and re-check data sources before deploying live capital.

Learning Resources

Open Source Code

Browse the full advanced time series toolkit on GitHub. Every chapter includes forecasting scripts, backtests, and utilities.

Run the resource-friendly Chapter 1, 2, 3, 6, and 7 notebooks directly in your browser.

LSTM (Chapter 4) and XGBoost (Chapter 5) are intentionally excluded to avoid heavy GPU/CPU usage,

and backtests are removed so you can focus on diagnostics from the lecture slides.

Parameters:

Running...

Results

Execution Time: seconds

Error:

Get in touch

If you have any questions or suggestions about the project, please feel free to contact us.